WED Vol. 1, Issue 1

Global factors continue to drive inflation in Canada. Domestically, the unexpected surge of residential real estate prices has also played an influential role in driving inflation higher.1

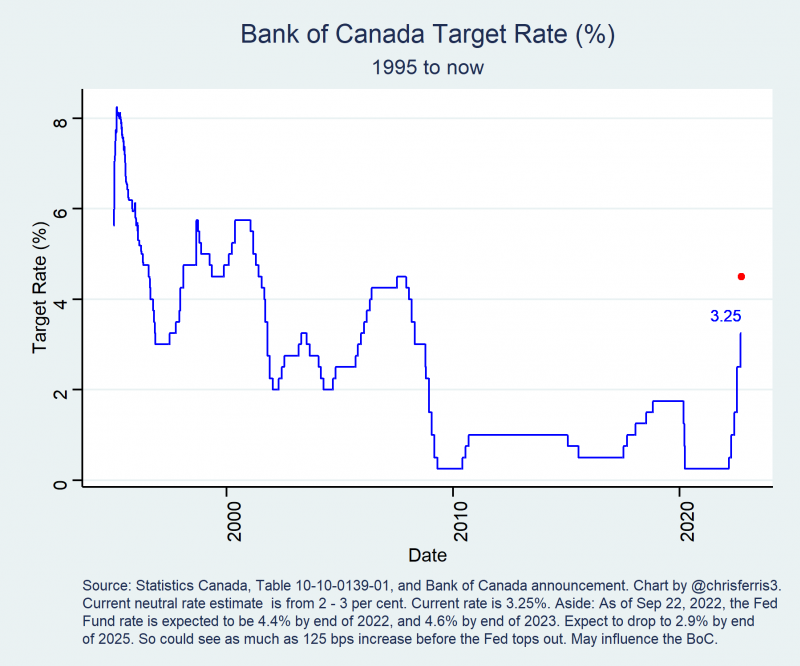

Combined with the broadening of price increases, and the desire to keep inflation expectations well anchored encouraged the Bank of Canada to raise its policy rate by 100 basis points on July 13, 2022, to 2.5 per cent.

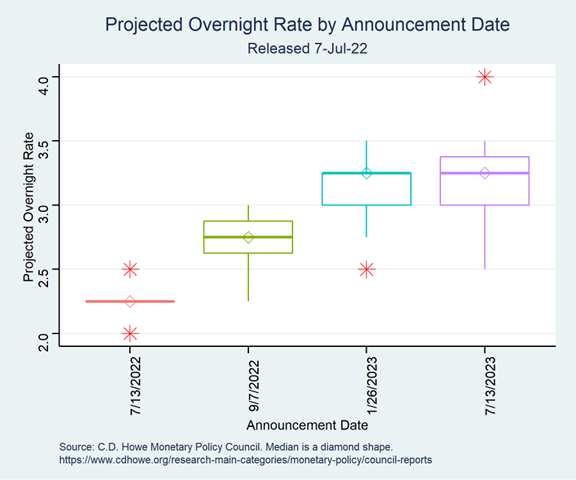

The C.D. Howe Monetary Policy Council vote on July 7, 2022, was for the Bank of Canada to raise their policy rate to 3.25 per cent by January 2023 and to hold there.

This means Manitoba households and organizations need to factor in at least another increase of 75-basis points on top of the 2.50 per cent rate that was announced on July 13, 2022. They should be having conversations with advisors (e.g., banker, accountant) sooner rather than later so they have time to adjust before interest rates bite even harder.

Analysis - Global Factors

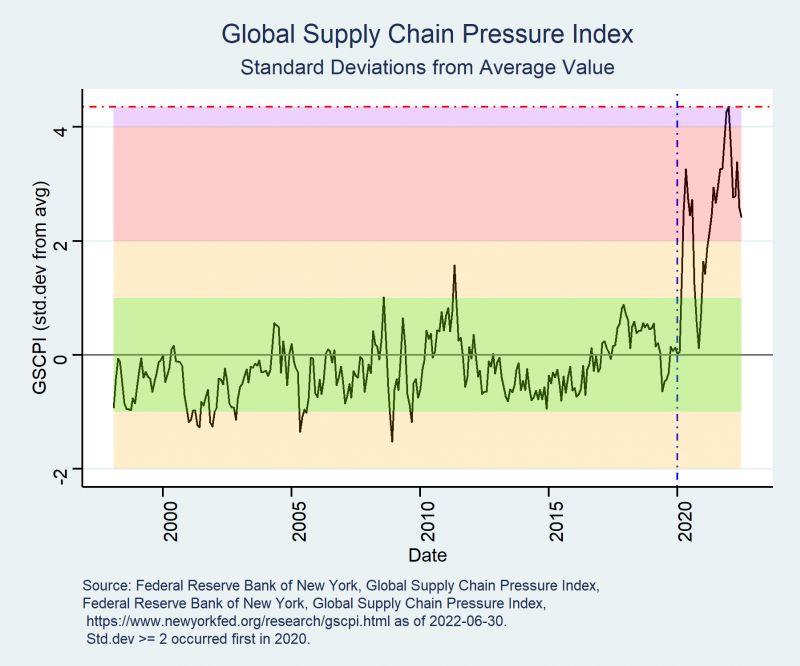

To get a blended view of major players in the global economy, the New York Fed put together a new index. The New York Fed’s Global Supply Chain Pressure Index (GSCPI) through June 2022 has dropped to 2.41 Standard Deviations (SD), off 45 per cent from its index high of 4.35 SD in December 2021.2 We are not out of the woods until we see the index drop below two SD and stay there for some time.

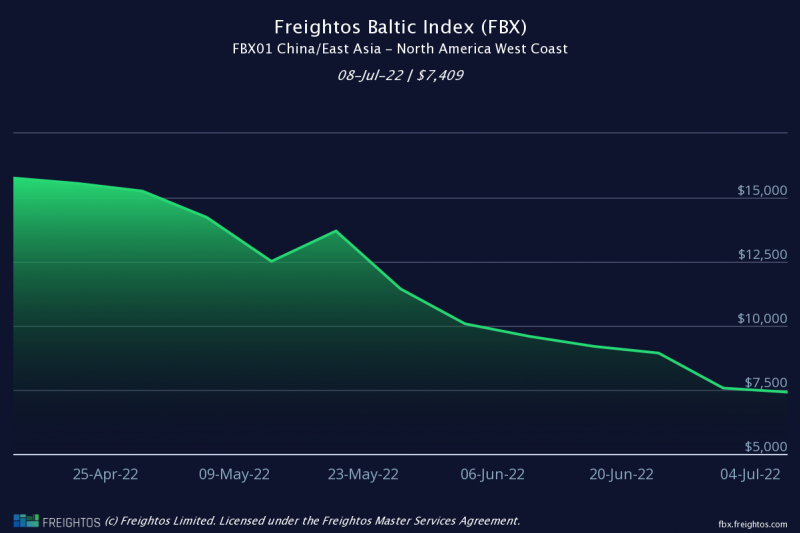

China has a consequential position in global value chains, so its continued use of harsh lockdowns for COVID-19 outbreaks, have all contributed to longer lasting supply chain disruptions. Still, shipping congestion and supply constraints are easing after a long lockdown that hit Shanghai in Q2 2022. Container shipping prices from East Asia to the West Coast of North America have been falling.

According to Freightos, average container prices FBX01 (China/East Asia – North America WC) have fallen 53 per cent from $15,764/day on April 15, 2022, to $7,409/day on July 8, 2022. The reverse trip FBX02 (North American WC – China/East Asia) has risen 4 per cent over the same period.

The July 8, 2022, the price ratio of daily rates: $7,409/$1,054 (7:1) still favours supplying shipping capacity to the FBX01 leg of the journey, but the ratio has become more balanced since May 20, 2022, when it was 16.5/1.

The ongoing Russian invasion of Ukraine (and harsh sanctions on Russia) continue to have disruptive effects on prices of crops, fertilizers, energy and numerous minerals. The EU and importers of Ukraine’s grain and oilseeds are particularly affected by the war.

While the outcome of the invasion is unknown, some of the uncertainty has eased.

Inflation: Canada, Manitoba, and Winnipeg CMA

Statistics Canada released the May 2022 Consumer Price Index on June 22, 2022. May 2022 inflation rose versus April 2022 inflation.

| Geography | Y/Y CPI Inflation (per cent) | |

|---|---|---|

| April 2022 | May 2022 | |

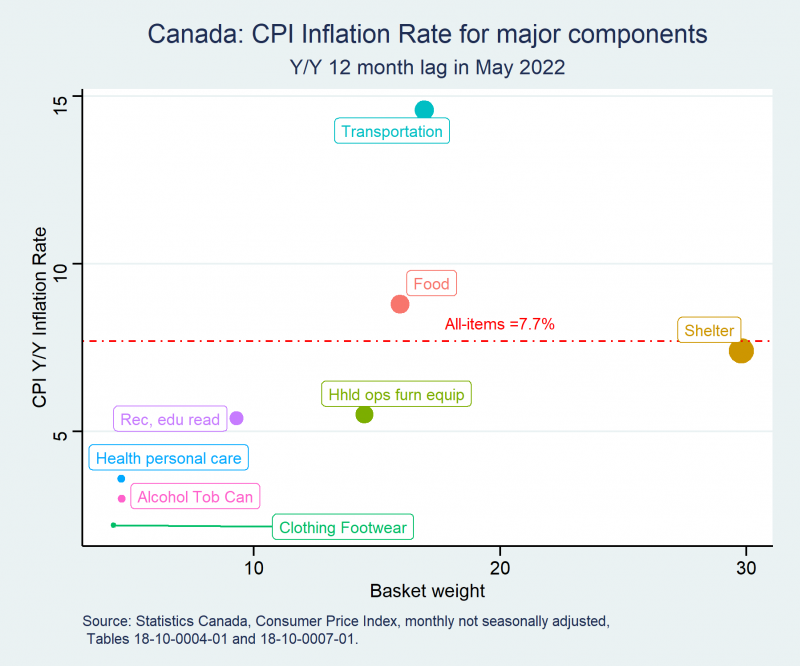

| Canada | 6.8% | 7.7% |

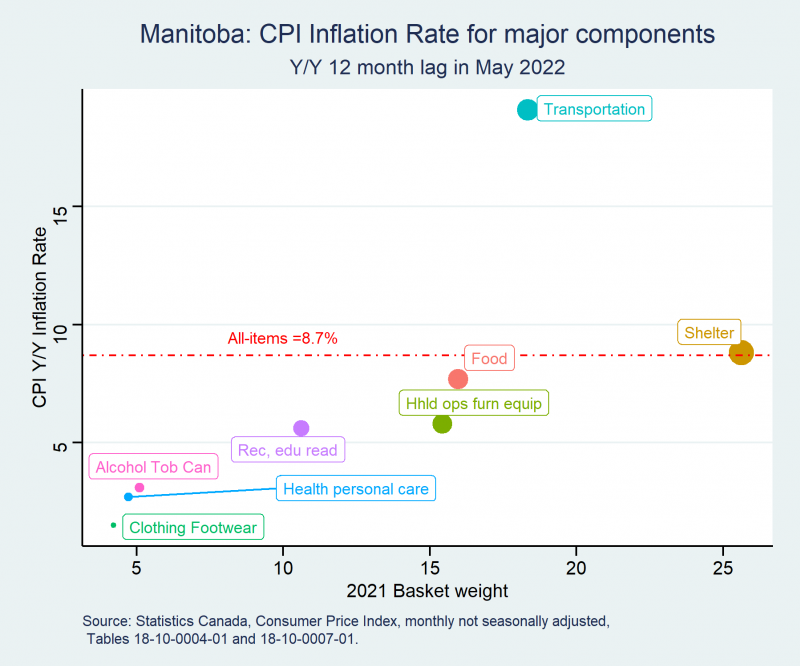

| Manitoba | 7.5% | 8.7% |

| Winnipeg CMA | 7.2% | 8.5% |

CPI inflation is being driven higher by transportation, food and shelter for both Canada and Manitoba.

We expect June 2022 inflation numbers to be comparable to the May 2022 numbers.

When it comes to transportation inflation for July 2022, we may have seen a peak. For example, WTI August’22 futures (CLQ22) fell from its contract high of US$121.44/bbl on June 14, 2022 to an intraday price US$93.74/bbl on July 14, 2022 (down 23%). Gasoline prices at the pump have begun to ease as well.

In regional markets, resale prices of housing have begun easing with the sharp increase in the overnight rate. For example, Winnipeg saw average prices fall month-over-month for detached and attached housing. This likely pushed some buyers into the condo market, adding support to average condo prices m/m. Rate hikes are expected to further cool the residential real estate market.

| Average Prices | May 2022 | June 2022 | Percentage Change (M/M) |

|---|---|---|---|

| Detached | $454,832 | $426,541 | -6.2% |

| Attached | $358,087 | $339,230 | -5.3% |

| Condos | $261,910 | $278,266 | +6.2% |

Food prices cannot react as quickly as transportation and shelter, due to biological restrictions to crops and livestock production along with weather.3

When we consider the two major sub-components of CPI food in May 2022, food store inflation and restaurant price inflation is lower in Manitoba than Canada overall.

| May 2022 Y/Y Inflation | Canada (%) | Manitoba (%) |

|---|---|---|

| Food Stores | 9.7 | 8.8 |

| Restaurants | 6.8 | 4.8 |

Bank of Canada’s July 13, 2022, interest rate announcement

On July 7, 2022, the C.D. Howe Monetary Policy Council (MPC) called for a 75-basis point increase to 2.25 per cent on July 13. They also called for a further 50-basis points increase on September 7 to 2.75 per cent. It’s also calling for an interest rate of 3.25 per cent by the January 2023 announcement date and staying at that level through July 2023.

As we know from the Bank of Canada’s July 13, 2022, announcement, the Bank of Canada (BoC) raised its overnight rate by 100 basis points, exceeding expectations. The BoC wants to prevent inflation expectations from becoming unmoored from the two per cent target.

Most of the C.D. Howe’s MPC members are calling for quantitative tightening (QT) to stay at its announced pace. The Bank of Canada (BoC) expects to roll off about 40 per cent of bonds over the next two years. Its total assets were $487 billion at the end of March 2022, so this would result in the balance sheet shrinking to approximately $292 billion in two years' time.4 Other major central banks are in a comparable situation of having to shrink their balance sheets.5

Inflation Forecast Review

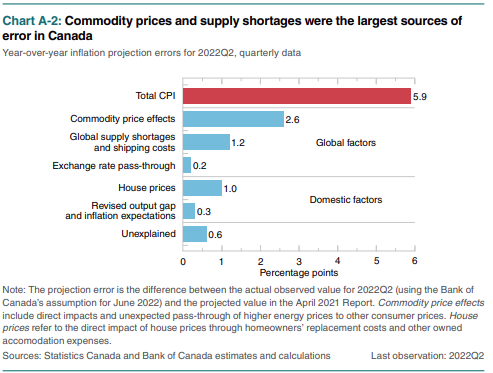

Many central banks have under-forecast inflation lately, and much of it is due to global effects. In the July 2022 Monetary Policy Review (MPR), the BoC published its analysis of what factors were most responsible for its under-forecast of inflation (see Chart A-2 from page 27 of the MPR). Global factors were estimated to be 68 per cent of the error, domestic factors 22 per cent, and 10 per cent were considered unexplained.

Will this tightening cycle result in a hard or soft landing?

Some commentators have shown skepticism about the BoC being able to achieve a soft landing. Of course, the BoC is not the only central bank in the world, so we can draw on the lessons of similar situations from around the world. A recent report by the Bank for International Settlements by Boissay et al,6 says soft landings involve smaller, shorter and more front-loaded rate hikes.

What degree of front-loading do we have in this tightening cycle?

The degree of front-loading is measured as the percentage of the overall hike that happens within the first two quarters of the tightening cycle. Before the rate hike cycle began in Canada, we were at 0.25 per cent. If we take the C.D. Howe MPC median rate expectation of 3.25 per cent as our peak, then the rate hike would be 300 basis points overall. With the current rate at 2.50, the rate hike to-date is 225 basis points.7 Thus, the degree of front-end loading to date is 225/300 or 75 per cent. We can expect to see at least 75 basis points of increase by the January 2023 rate announcement.

Threading the needle will remain a challenge, but by front-end loading rate increases during the current tightening cycle, the odds of a softer landing are improved.

____________________

- Shelter's weight is 30% of the Canadian CPI, and 25% of Manitoba's CPI.

- The GSCPI blends information on the Baltic Dry Index, Harpex index, air freight costs indexes from the BLS of the USA, and supply chain related components from Purchasing Managers’ Index surveys for manufacturers in China, the euro area, Japan, South Korea, Taiwan, the UK, and the USA. This index shows the standard deviation (SD) from the average value. The GSCPI starts on Jan 1998, with monthly measures through June 30, 2022.

- The ongoing invasion by Russia of Ukraine disrupting production and shipping for crops in Ukraine will continue to keep upward pressure on crop prices for some time yet. Droughts and high temperatures are likely to challenge some major crop production zones around the world as well.

- Source: Statistics Canada: Table 10-10-0108-01.

- Central Banks had used quantitative easing when their rates hit their lower bound. This helped prevent financial markets from seizing up and economies from cratering in the early days of the COVID-19 pandemic (Q1/Q2 2020).

- Boissay et al (July 14, 2022) “Hard or soft landing?” BIS Bulletin Number 59. Hard or soft landing? (bis.org). Graph 2 on page 3 of the report. Comes from a study of 70 tightening episodes across 25 countries over the period 1980 – 2019.

- The current overnight rate of 2.50 per cent is within the neutral rate estimate of 2 to 3 per cent.